When administering an estate, one of the most important responsibilities of an executor—formally known as a Personal Representative—is identifying exactly what must be included in probate. Under the Trustee Act 2000, you are subject to a statutory duty of care to act as a "prudent person of business," ensuring the estate is managed honestly and accurately.

It is a common misconception that only property and bank accounts need to be declared. In reality, almost all assets owned solely—or sometimes jointly—by the deceased must be valued and reported to provide a complete and accurate account for HM Revenue & Customs (HMRC). Failure to do so can lead to personal liability for delays, interest, or penalties.

What Must Be Included in Probate?

In general, probate covers all assets owned by the deceased at the date of death. The list includes:

1. Property

- Main residence, buy-to-let properties, and holiday homes.

- Land and development plots.

- Overseas property, especially if the deceased met the long-term UK residence test (resident for 10 of the last 20 tax years), as they are liable for Inheritance Tax (IHT) on their worldwide estate.

- Each property must be valued at its open market value at the date of death, not an insurance rebuild figure or an estate agent’s asking price.

2. Bank Accounts & Savings

- Current and savings accounts, ISAs, and Premium Bonds.

- The total reported must be net of funeral expenses and debts outstanding at the date of death. Under the Finance Act 2013, a debt is generally only deductible if it is actually repaid to the creditor from the estate.

3. Investments

- Stocks, shares, unit trusts, and investment portfolios.

- Cryptocurrency holdings and other digital assets, which must be accounted for in modern estate planning.

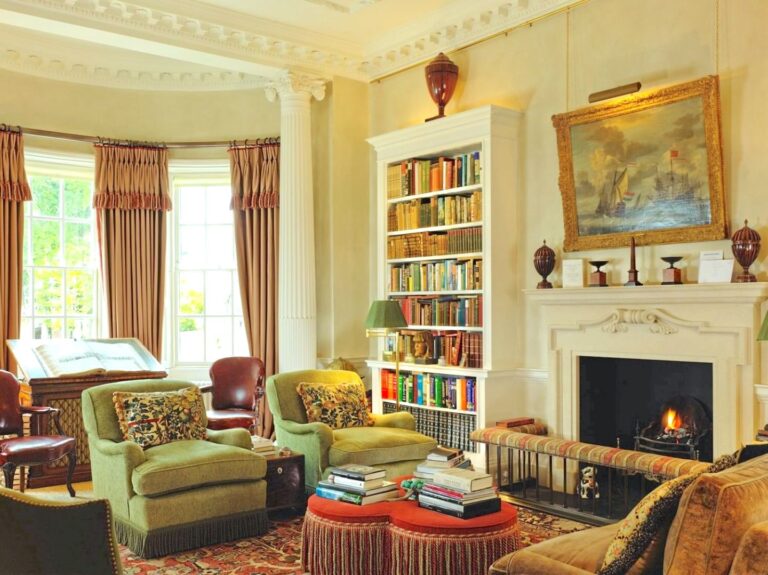

4. Personal Chattels (Personal Possessions & Household Contents)

In legal terms, "chattels" refers to all tangible movable property. This is the area most commonly overlooked. Items that must be included are:

- Jewellery and watches

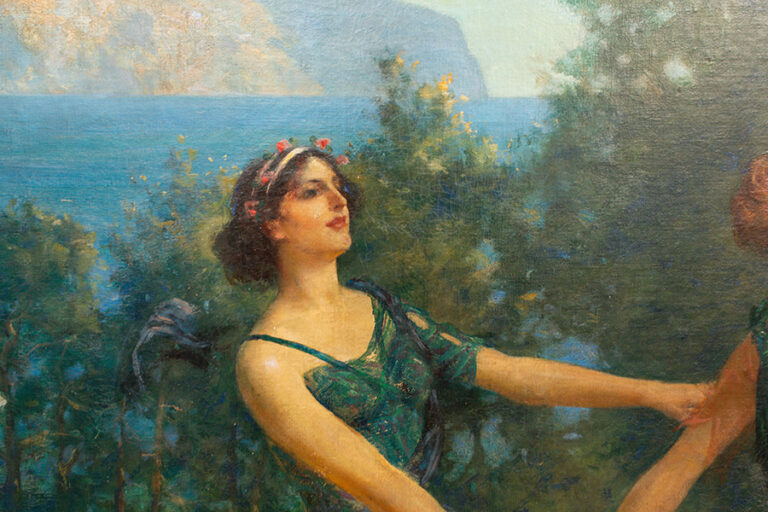

- Fine art and paintings

- Antiques

- Silver

- Collectables (coins, stamps, memorabilia, wine, etc.)

- Designer handbags and luxury goods

- Vehicles

- General household contents Importantly, these must be valued at a realistic second-hand market value (open market value) as of the date of death, not the original purchase price or insurance replacement cost. Be aware that Capital Gains Tax (CGT) may also apply to gains from the disposal of personal chattels.

5. Business Interests

- Sole trader businesses, partnerships, and limited company shares.

- These may qualify for Business Relief (BR), which can reduce the asset’s taxable value by 50% or 100%. However, from April 2026, a £1 million cap will apply to these combined reliefs per individual.

6. Pensions (In Certain Circumstances)

- While many pensions currently fall outside the estate, unused pension funds and death benefits are scheduled to be brought into the IHT net starting in April 2027.

7. Life Insurance Policies

- Policies that pay into the estate must be included.

- Policies written in trust typically fall outside the estate for probate purposes.

8. Trust Interests

- If the deceased had a qualifying interest in possession (IIP) or an Immediate Post-Death Interest (IPDI) in a trust, the underlying capital value of that trust is often aggregated with their own estate for IHT purposes.

9. Money Owed to the Deceased

- Personal loans made to others, unpaid salaries, dividends, and tax refunds. Even if you intend to "forgive" a debt in your Will, the value of that loan is still an asset that must be reported to HMRC.

What About Jointly Owned Assets?

Joint assets must be reported, but their treatment depends on how they were legally held:

- Joint Tenants: The asset passes automatically to the survivor by survivorship regardless of a Will.

- Tenants in Common: The deceased’s share does not pass automatically and must be distributed according to the Will or intestacy rules.

What Is Often Missed?

Executors frequently overlook:

- Gifts made within 7 years of death: These "failed" potentially exempt transfers (PETs) must be added back to the estate total to calculate IHT liability.

- Valuable items stored in lofts, garages, or drawers, such as high-value watches or wine collections.

- Digital assets, such as online investment accounts or social media legacies.

Why Accurate Inclusion Matters

Every item included determines the total net value of the estate, which dictates:

- Whether Inheritance Tax (IHT) is payable (usually at 40% above the available Nil-Rate Bands).

- Whether the estate qualifies as "excepted" or requires full IHT400 reporting.

- Your protection as an executor; failing in your statutory duty of care through negligence or omitting assets can lead to personal liability for penalties and interest.

Do You Need Professional Help?

Identifying and valuing estate contents correctly is challenging. Personal Representatives are legally entitled to take "proper advice" from qualified experts at the expense of the estate. Professional involvement ensures:

- All relevant assets (including trust interests and worldwide property) are accounted for.

- Defensible open market values are applied to satisfy HMRC and create an audit trail.

- The executor is protected from future disputes or HMRC enquiries.

Please note: This article does not constitute financial advice.

Related Articles

How HMRC Assesses Probate Valuations

How To Establish the Value of an Estate

The Importance of Accurate Probate Valuations

If you are currently dealing with an estate and require a probate valuation, Dawsons Auctioneers provide professional, HMRC-compliant reports for executors, solicitors and families across the UK. Our specialists assess house contents, jewellery, art and antiques, offering clear guidance and transparent fees throughout the process.

If you would like further information or to speak to a specialist, you can explore our services or get in touch with our team.